DORA private banking: the real test arrives with the 2026 resilience tests

Applicable since January 2025, DORA triggers its hardest obligations in 2026: TLPT operational resilience tests and a register of critical providers.

Retail banks, neobanks and financial institutions need explainable credit scoring, robust back-office, real-time fraud detection and auditable DORA / Basel IV compliance. Swoft natively delivers the immutable audit trail required by ACPR and the ECB.

Before talking software, we talk pain points. If you don't recognize any of these three, we are probably not the right partner for you.

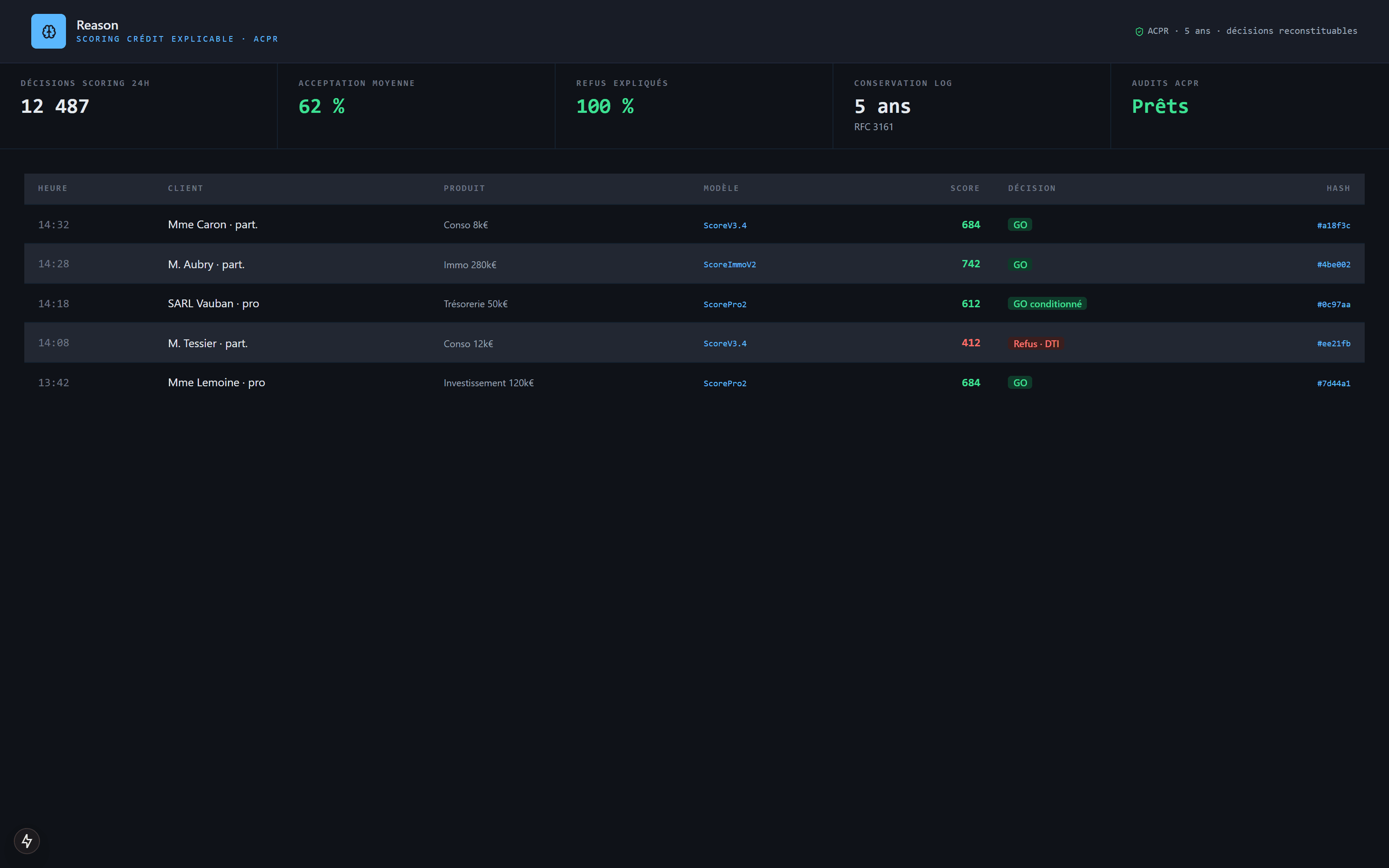

Your scoring models run in production, but when the regulator asks why customer X was refused credit on 12 March 2024, you cannot replay the decision. Major regulatory risk post EU AI Act.

0 traceability of AI decisions on most core systems

Subscriptions, refunds, transfers, claims: sequential processes with overnight batches, no consistency guaranteed on partial failure. Manual corrections drift, LPs complain.

Overnight batches = 8h+ of consistency latency

Fines up to 10% of annual revenue for non-compliant EU financial actors. Most core systems lack native operational-resilience evidence, only controls layered on top.

DORA fines up to 10% of annual revenue

When your processes require a replayable audit trail, sagas with compensation, or compliance by construction, we ship an event-driven architecture (DDD + CQRS + Event Sourcing), not a CRUD layered with audit logs.

Every scoring decision is kept with full reasoning, model used, confidence score, input data and model version. Replayable identically five years later for the regulator, patented "AI Decision as Data" mechanism (ADR-120).

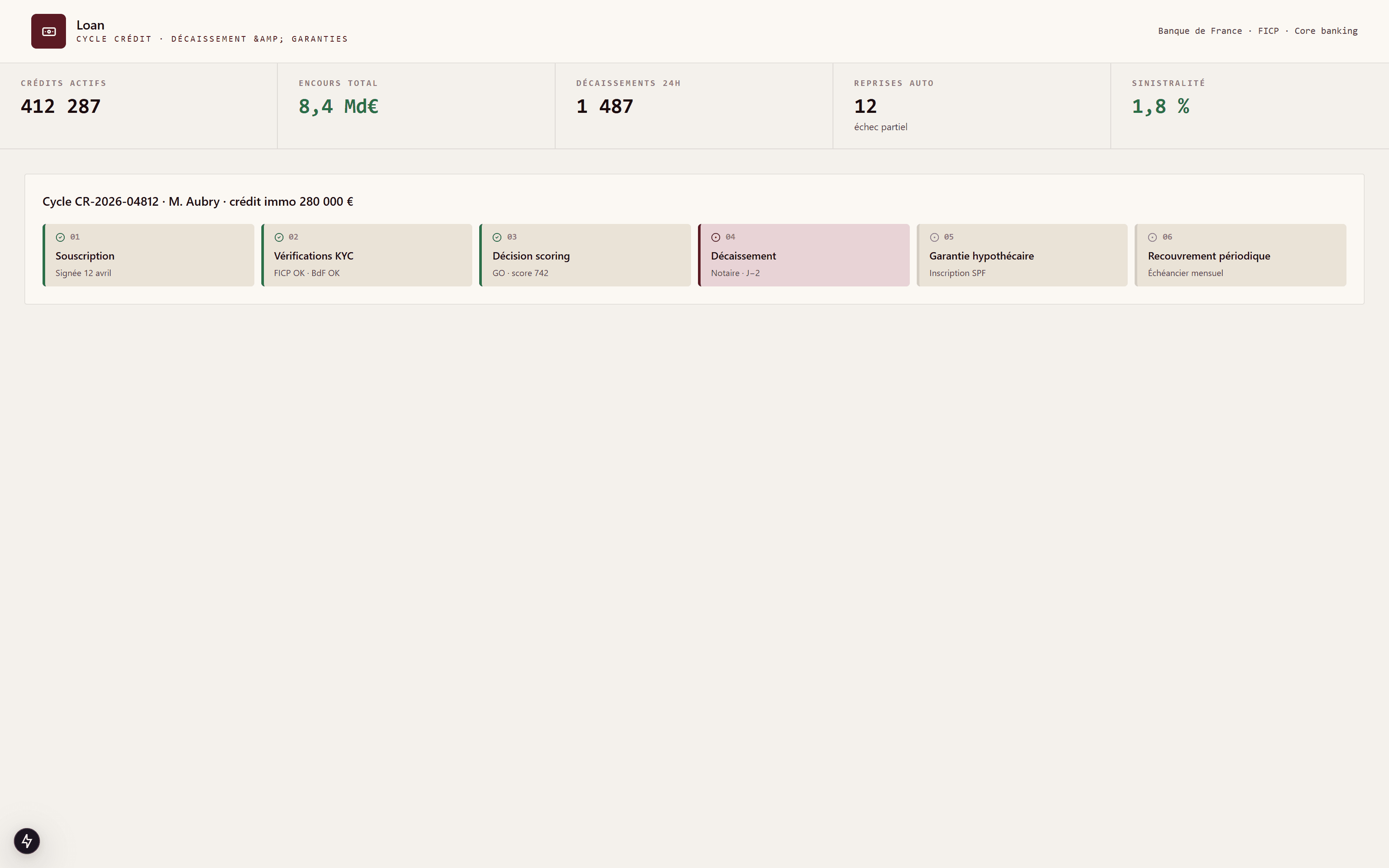

Full cycle for retail or business credit: subscription → checks → decision → disbursement → guarantees → recovery, with clean recovery on partial failure. Human validation steps on files above the delegation threshold. State is never corrupted, designed for DORA-critical transactions.

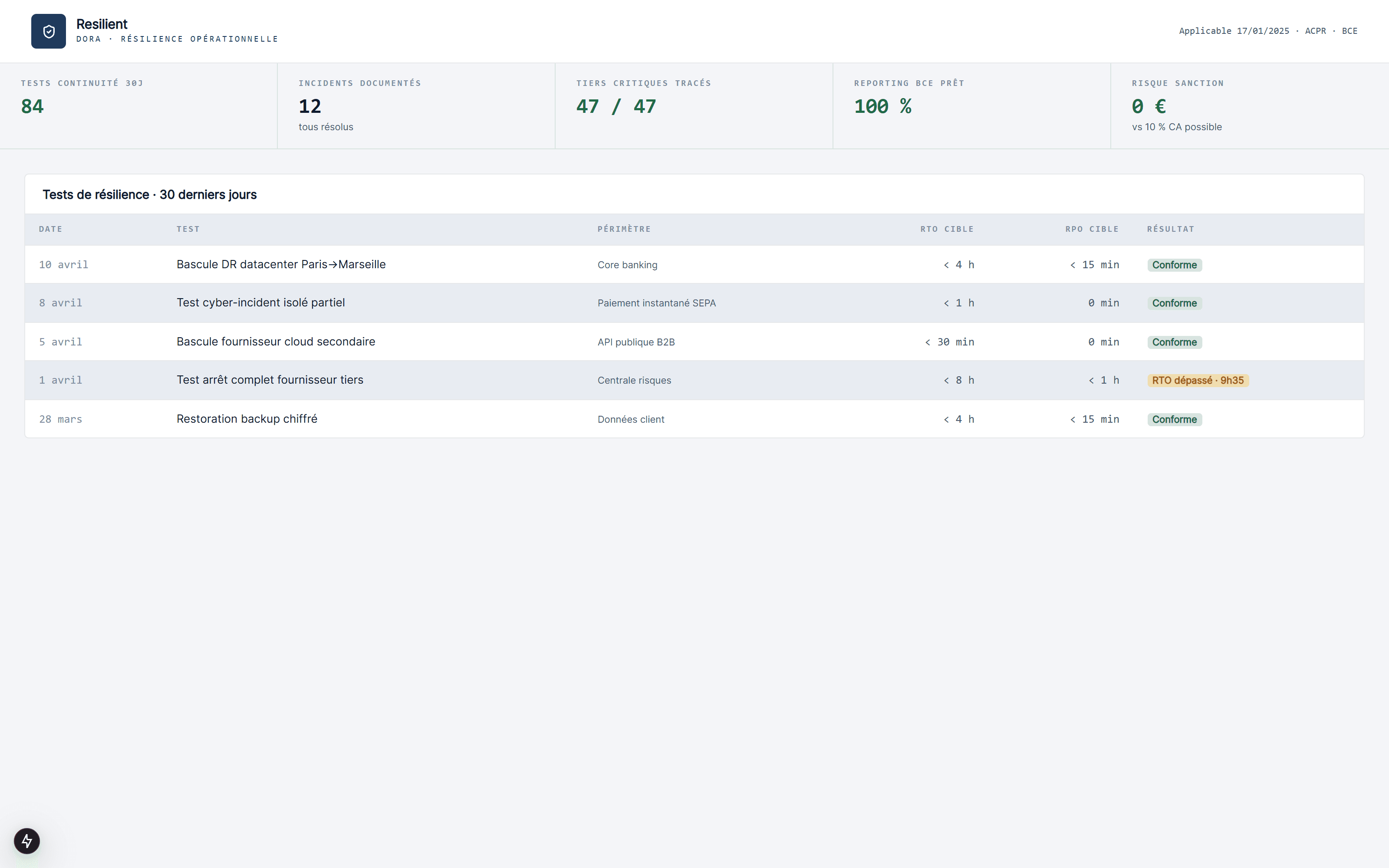

Tamper-proof history of every system action, automated operational-continuity tests, incident register, regulator reporting in a few clicks. Compliant with DORA from first deployment, EU fines up to 10% of revenue avoided.

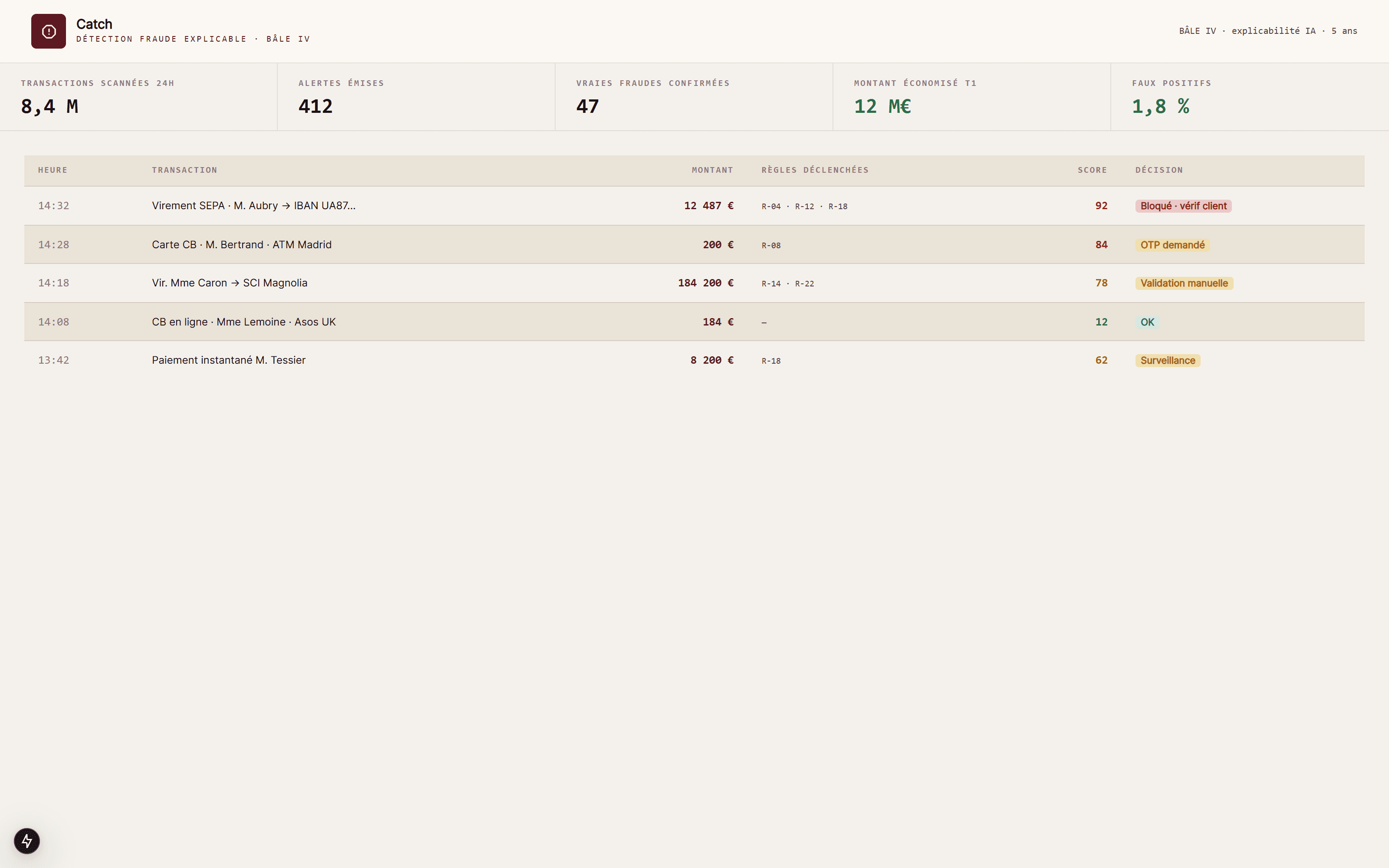

Every fraud alert is kept with its score, triggered rules and AI reasoning. The decision is frozen, never re-executed after the fact. Meets the Basel IV model-explainability requirement, tamper-proof evidence by construction.

For everything else (CRM, portals, scheduling, billing), we ship a custom application, on your design system and with your existing integrations.

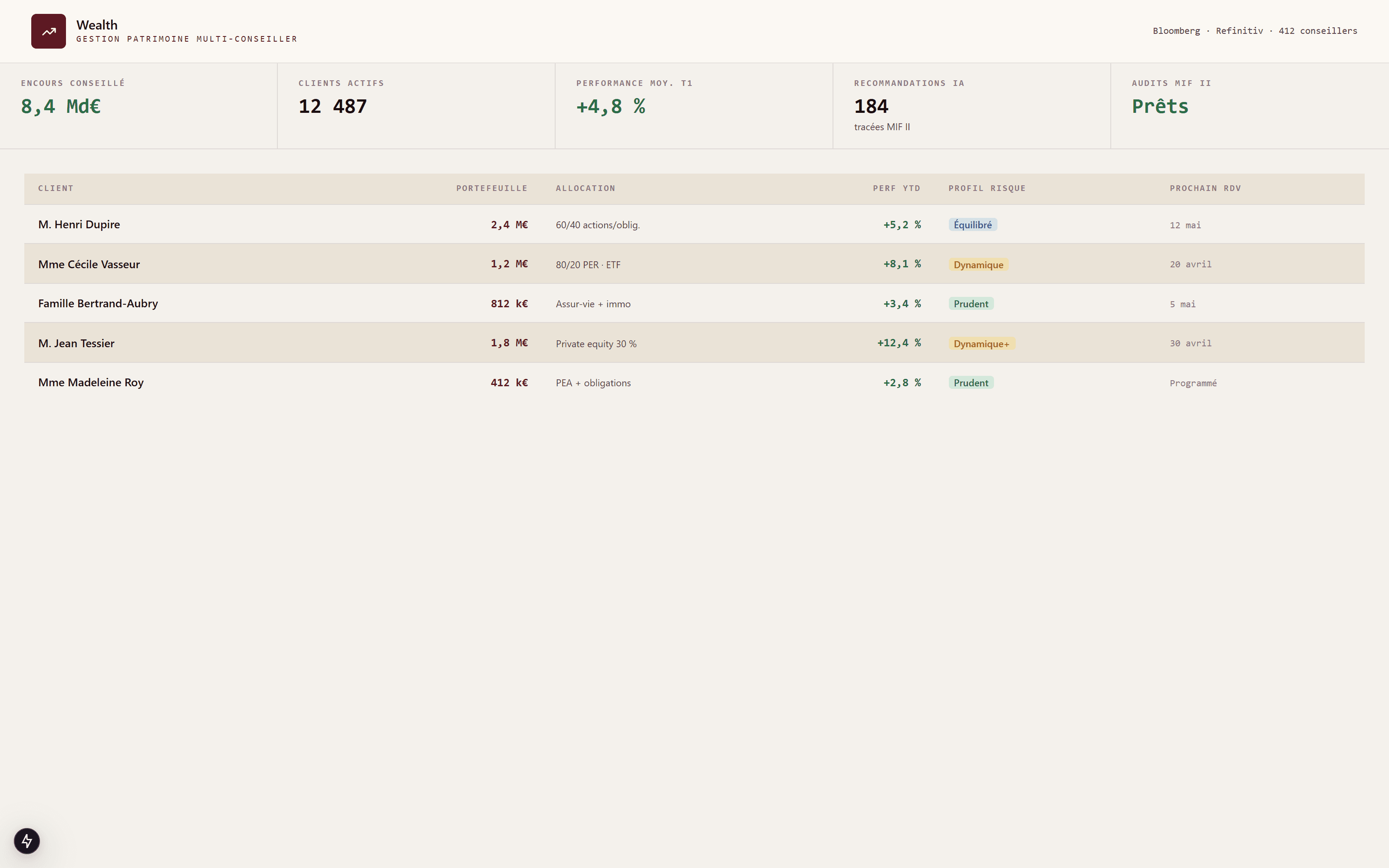

CRM + portfolio + traced AI recommendations. Per-advisor compartmentalized (isolated DB), MiFID II audit reconstructed directly from history. Structured KYC/AML onboarding.

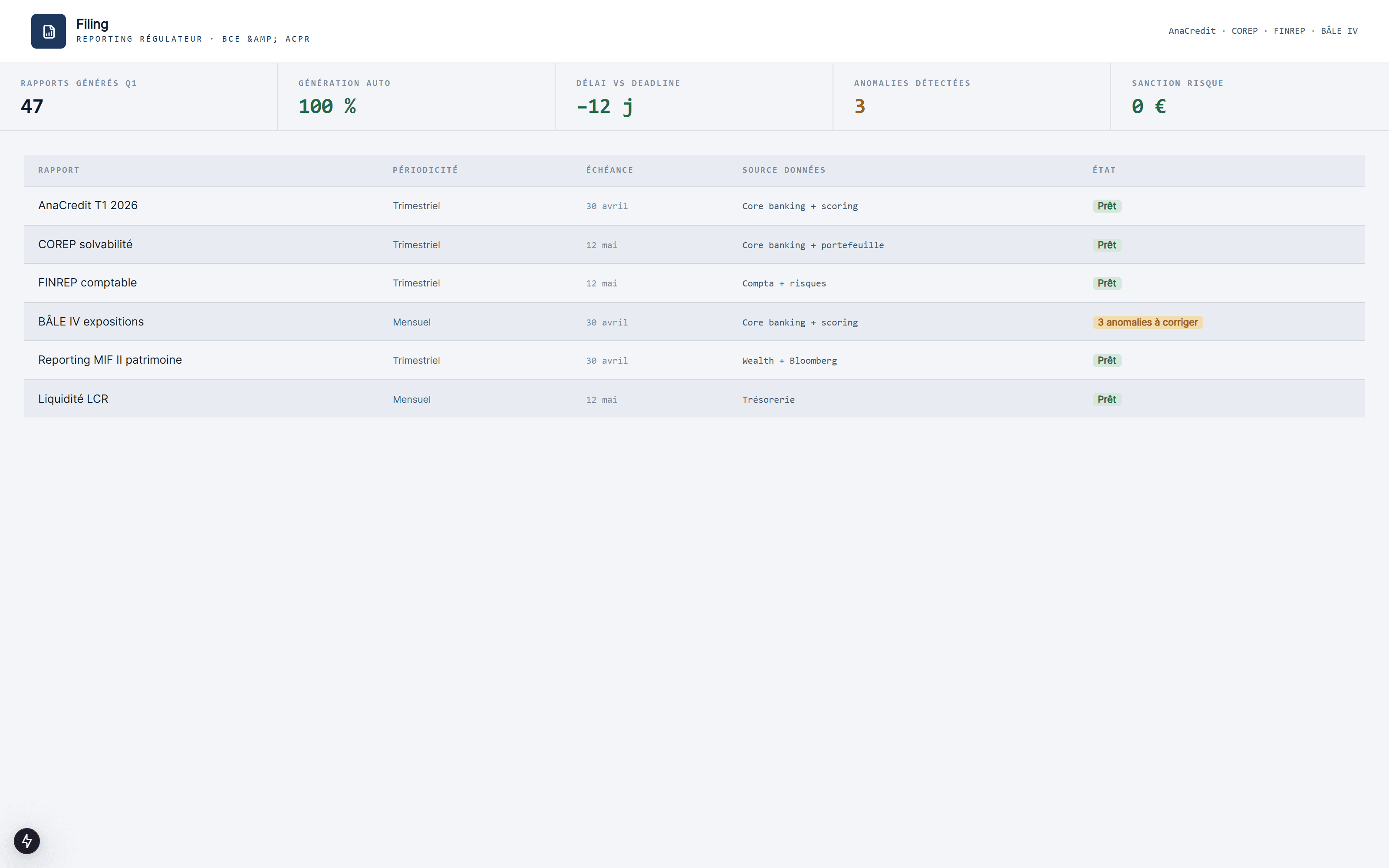

AnaCredit, COREP, FINREP, Basel IV reporting automatically generated from regulatory history. No after-the-fact reconstruction, no fragile batch.

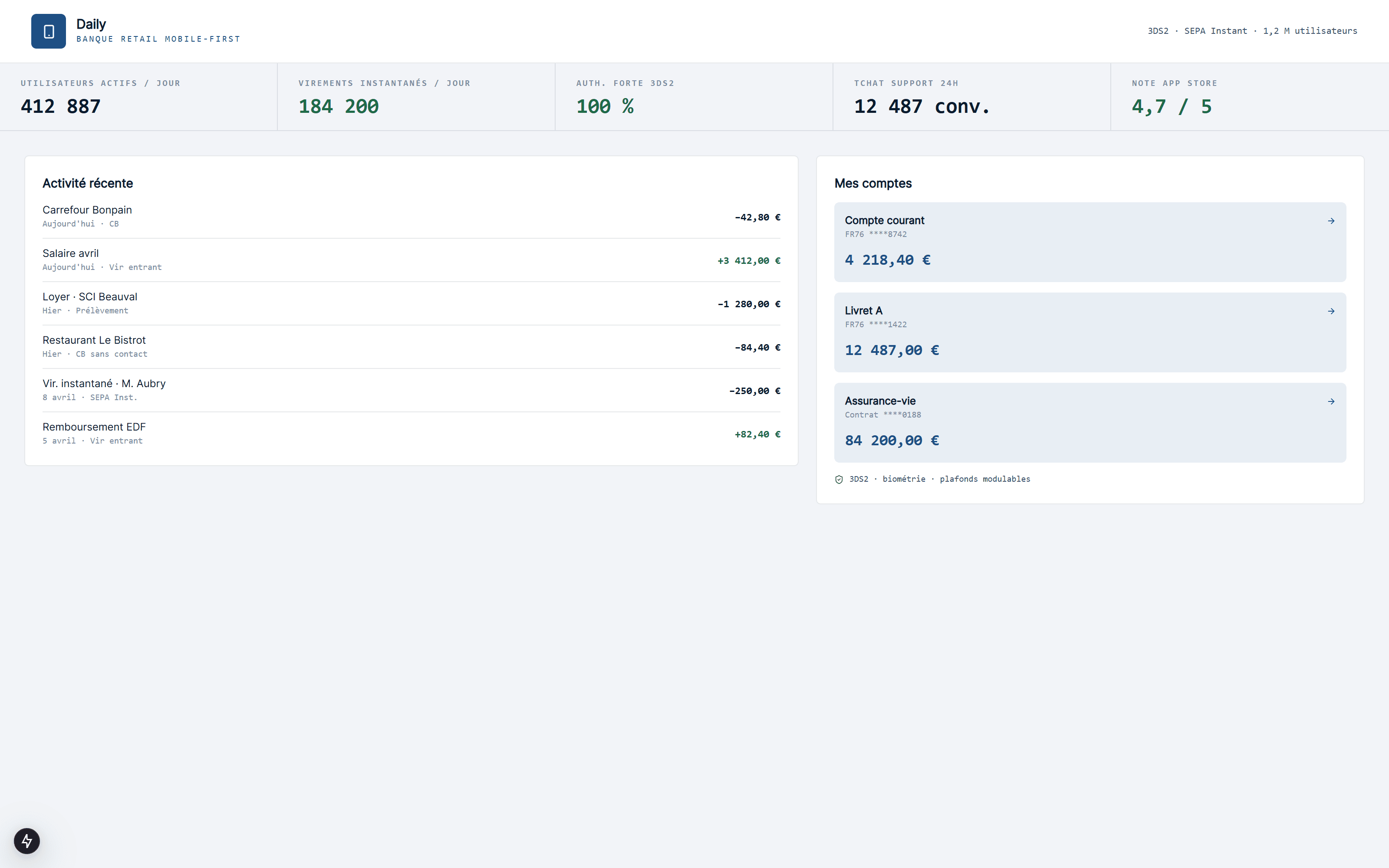

Mobile-first customer space with instant SEPA transfers, payment-method management, limit configuration, chat support. Strong 3DS2 authentication.

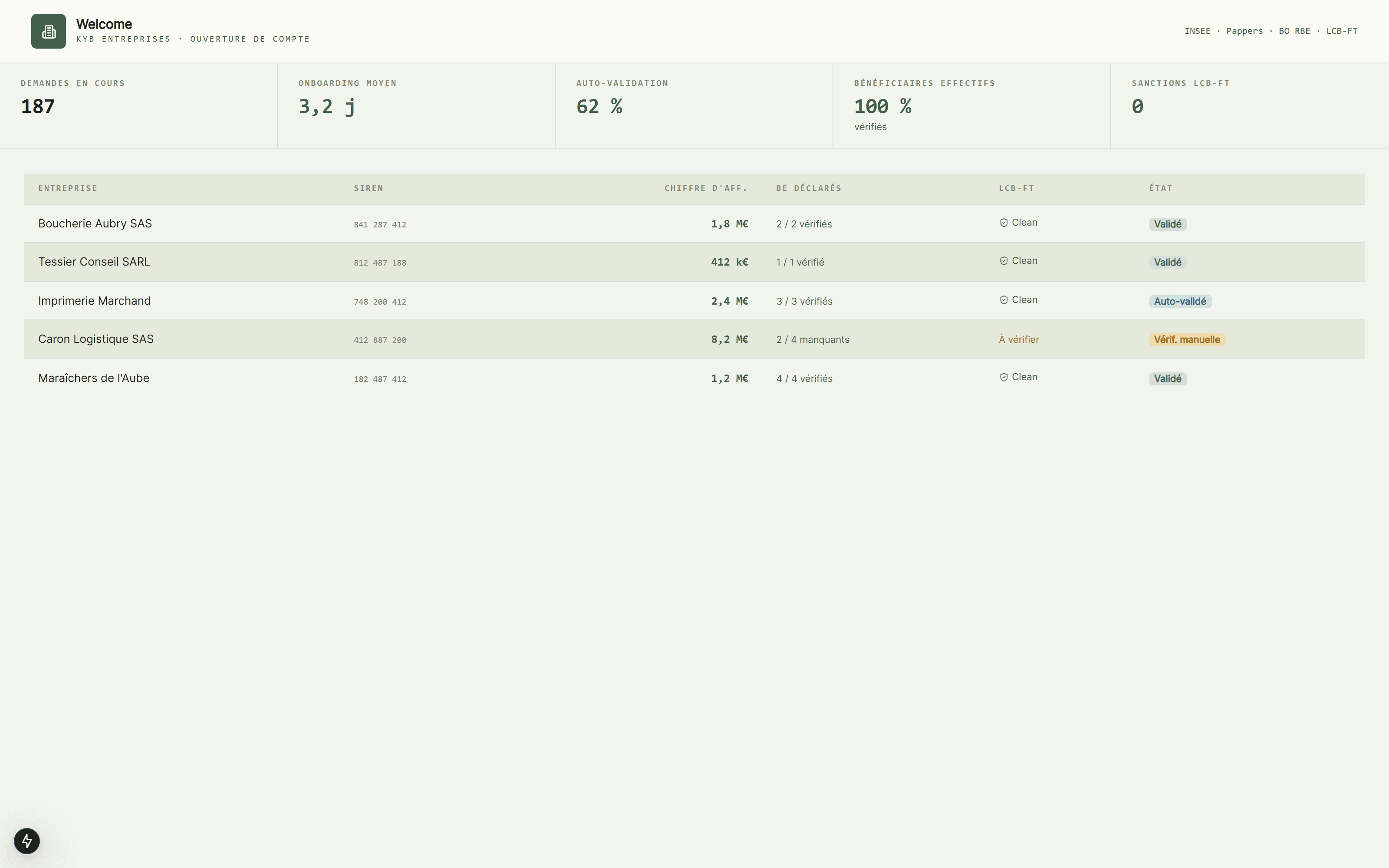

Business account-opening journey with integrated KYB: INSEE, BODACC, Pappers retrieval, automatic scoring, electronic signature of terms. Opening time cut from 2 weeks to 48 hours.

Business compliance and key integrations are not options, they are prerequisites built in from the start.

Digital operational resilience, applicable 17 January 2025

Prudential requirements, model auditability

Financial supervision, evidence of automated decisions

Investment services, wealth management

Personal data, multi-tenant with isolated DB

Applicable 2 August 2026, high-risk systems art. 8-15

Mixed firms (accounting + audit, accounting + advisory, accounting + legal) draw from several industries. Here are those that share the most challenges.

Réglementations, virages business, sous-domaines en mutation : ce que notre pôle veille publie sur le secteur Banking.

Applicable since January 2025, DORA triggers its hardest obligations in 2026: TLPT operational resilience tests and a register of critical providers.

Les réglementations qui pèsent sur les choix logiciels (appliquées, partielles, ou imminentes), décryptées par notre pôle veille.

Network and Information Security 2, Directive (UE) 2022/2555

Directive cybersécurité européenne applicable depuis octobre 2024. Élargit le périmètre aux SaaS, datacenters, transporteurs, alimentaire.

Digital Operational Resilience Act, Règlement (UE) 2022/2554

Règlement européen sur la résilience opérationnelle numérique du secteur financier. Applicable depuis le 17 janvier 2025, avec TLPT en 2026.

Corporate Sustainability Reporting Directive, Directive (UE) 2022/2464 et standards ESRS

Cadre européen de reporting de durabilité. Première vague 2024 (grandes entreprises), deuxième vague 2025-2026 pour les ETI > 250 salariés.

Règlement (UE) 2024/1689 sur l'intelligence artificielle

Premier cadre horizontal mondial de régulation de l'IA. Obligations IA haut risque applicables le 2 août 2026.

30 minutes with Derick (CTO, ex-BNP Paribas, Groupama, Meeschaert) to scope your need and price the solution.